Highlights

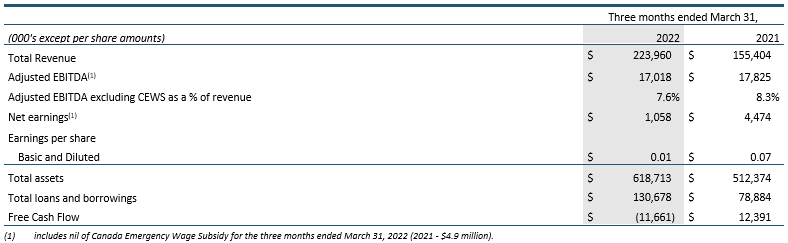

- Revenue of $224.0 million for Q1 2022 increased $68.6 million, or 44%, compared with Q1 2021 and $22.4 million compared to Q4 2021. The FCPI Dana Investments Inc. (“Dana”) and Tricom Group (“Tricom”) acquisitions in the quarter accounted for $25.2 million of the increase with the remainder primarily due to strong WAFES results related to high resource sector activity levels and new clients wins in 2021;

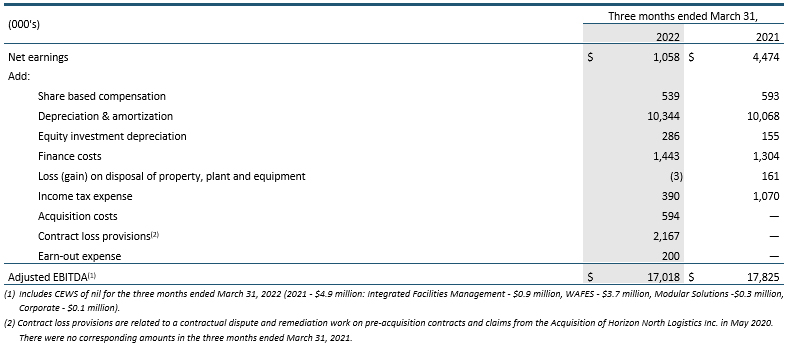

- Dexterra Group Inc.’s (“Dexterra Group” or the “Corporation”) Adjusted EBITDA for Q1 2022 was $17.0 million compared to $18.1 million in Q4 2021 which included an unusual one-time contract renegotiation fee of $1.8 million for WAFES. The strong IFM and WAFES results were offset by delays in rapid affordable housing projects, inflationary pressures, and start-up costs for a new product line in the Modular business;

- Net earnings were $1.1 million for Q1 2022 compared to consolidated net earnings of $4.5 million in Q1 2021. The Q1 2022 results included a provision for costs of $2.1 million associated with pre-acquisition Horizon North Logistics Inc. contract disputes and related remediation work;

- Debt increased in Q1 2022 to $130.7 million at March 31, 2022. Approximately $50 million of the increase is due to the acquisitions;

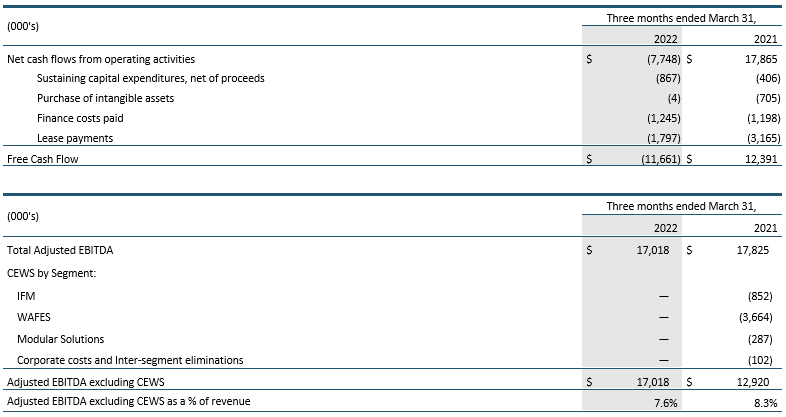

- The Free Cash Flow deficit of $11.7 million in Q1 2021 included a significant increase in trade receivables of $28.4 million, excluding the Dana acquisition, which related to higher sales and timing of client payments. The increase in trade receivables was temporary as days sales outstanding were significantly reduced in April. The Corporation expects its conversion of EBITDA to free cash flow to exceed 50% for fiscal 2022; and

- The Corporation declared a dividend for Q2 2022 of $0.0875 per share for shareholders of record at June 30, 2022, to be paid on July 15, 2022.

This news release contains certain measures and ratios, such as Adjusted EBITDA, Adjusted EBITDA excluding CEWS as a % of revenue, Free Cash Flow and Backlog, that do not have any standardized meaning as prescribed by GAAP and, therefore, are considered non-GAAP measures that do not have a prescribed meaning under IFRS. The method of calculating these measures may differ from other entities and accordingly, may not be comparable to measures used by other entities. See “Non-GAAP measures” and “Reconciliation of Non-GAAP measures” of the Corporation’s MD&A for the three months ended March 31, 2022 and 2021 for details which is incorporated by reference herein.

Toronto, Ontario, Canada, May 10, 2022 – TSX Symbol: DXT

First Quarter Financial Summary

First Quarter Operations Analysis

Integrated Facilities Management (“IFM”)

For Q1 2022, IFM revenues were $64.2 million and increased by $26.2 million, or 69%, from the $38.0 million in Q1 2021. The increase reflects the acquisitions of Dana and Tricom, which contributed $20.9 million and $4.3 million in revenue in Q1 2022, respectively. Excluding the acquisitions, revenue was flat with Q4 2021 which included higher special projects revenue.

Adjusted EBITDA, excluding CEWS as a percentage of revenue, is 6.2% for Q1 2022, which is lower than the 7% recorded in Q1 2021 and is consistent with Q4 2021. The IFM business, excluding the 2022 acquisitions, improved margins in Q1 2022 as Dana included some one time acquisition costs.

Workforce Accommodations, Forestry and Energy Services (“WAFES”)

Revenue from the WAFES segment for Q1 2022 was $115.1 million, an increase of $39.4 million compared to Q1 2021 and essentially flat with Q4 2021. WAFES revenue performance was strong in Q1 2022 due to increased camp occupancy and utilization across all services including catering, install, and rental activities as well as high access matting and space rental utilization in Energy Services.

The Q1 2022 Adjusted EBITDA excluding CEWS as a percentage of revenue is 14%, compared to 15% in Q1 2021 due primarily to revenue mix and the move to a greater percentage of support services work.

Modular Solutions

Modular Solutions segment revenues for Q1 2022 were $43.3 million compared to $41.9 million in Q1 2021 and $46.5 million in Q4 2021. Revenue was lower than expected due to client driven delays in affordable housing projects in Ontario and site access issues in the West due to the floods in British Columbia. Revenue is expected to rebound in Q2 2022 and through the balance of the year.

Adjusted EBITDA for Q1 2022 was $0.4 million compared to $2.9 million in Q1 2021 and $2.9 million in Q4 2021. Margins in Q1 2022 were primarily impacted by materials and subcontractor cost inflation on fixed price contracts and the lost margin and start-up costs of $1 million on a new manufacture-only modular product for US-based multi-family projects. The delays in affordable housing projects also impacted plant utilization resulting in lower overhead absorption.

Liquidity and Capital Resources

For the three months ended March 31, 2022, cash used by operating activities was $7.7 million, compared to cash generated of $17.9 million in the same period of 2021. The decrease in Q1 2022 primarily represents an increase in accounts receivable of $28.4 million, excluding the Dana acquisition, which was due to higher Q1 revenue and the timing of client payments. The conversion of EBITDA to free cash flow for 2022 is expected to exceed 50%.

Debt increased by $65.5 million in Q1 2022, which was primarily from funding the acquisitions and the working capital increase. Leverage approximates 1.6x 2021 Adjusted EBITDA. The Corporation’s financial position and liquidity remain strong with $59.2 million unused capacity on its credit lines at March 31, 2022.

Additional Information

A copy of Dexterra Group’s Condensed Consolidated Interim Financial Statements (“Financial Statements”) for the three months ended March 31, 2022 and 2021 and related Management’s Discussion and Analysis (“MD&A”) have been filed with the Canadian securities regulatory authorities and are available on SEDAR at sedar.com and Dexterra Group’s website at dexterra.com. The Financial Statements have been prepared in accordance with International Financial Reporting Standards and the reporting currency is in Canadian dollars.

Conference Call

Dexterra Group will host a conference call and webcast to begin promptly at 8:30 Eastern time on May 11, 2022 to discuss Dexterra Group’s first quarter results.

To access the conference call by telephone the conference call dial in number is 1-800-319-4610.

A live webcast of the conference call will be accessible on Dexterra Group’s website at dexterra.com/investor-presentations-events/ by selecting the webcast link. A PowerPoint presentation will be posted on Dexterra Group’s website at dexterra.com on May 10, 2022 to be reviewed on the conference call. An archived recording of the conference call will be available approximately one hour after the completion of the call until June 11, 2022 by dialing 1-855-669-9658, passcode 8639.

About Dexterra Group

Dexterra Group employs more than 7,500 people, delivering a range of support services for the creation, management, and operation of infrastructure across Canada.

Powered by people, Dexterra Group brings best-in-class regional expertise to every challenge and delivers innovative solutions, giving clients confidence in their day-to-day operations. Activities include a comprehensive range of integrated facilities management services, industry leading workforce accommodation solutions, innovative modular building capabilities, and other support services for diverse clients in the public and private sectors.

For further information contact:

Drew Knight, CFO

Head office: Airway Centre, 5915 Airport Rd., 4th Floor Mississauga, Ontario L4V 1T1

Telephone: (416) 767-1148

You can also visit our website at dexterra.com.

Reconciliation of non-GAAP measures

The following provides a reconciliation of non-GAAP measures to the nearest measure under GAAP for items presented throughout the News Release.

Forward-Looking Information

Certain statements contained in this news release may constitute forward-looking information under applicable securities law. Forward-looking information may relate to Dexterra Group’s future outlook and anticipated events, business, operations, financial performance, financial condition or results and, in some cases, can be identified by terminology such as “continue”; “forecast”; “may”; “will”; “project”; “could”; “should”; “expect”; “plan”; “anticipate”; “believe”; “outlook”; “target”; “intend”; “estimate”; “predict”; “might”; “potential”; “continue”; “foresee”; “ensure” or other similar expressions concerning matters that are not historical facts. In particular, statements regarding Dexterra Group’s future operating results and economic performance, including COVID-19 related impacts and the impacts of the Dana and Tricom acquisitions; its leverage, Free Cash Flow, NRB Modular Solutions backlog and revenue, and its objectives and strategies are forward-looking statements. These statements are based on certain factors and assumptions, including expected growth, results of operations, performance and business prospects and opportunities regarding Dexterra Group, which Dexterra Group believes are reasonable as of the current date. While management considers these assumptions to be reasonable based on information currently available to Dexterra Group, they may prove to be incorrect. Forward-looking information is also subject to certain known and unknown risks, uncertainties and other factors that could cause Dexterra Group’s actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by such forward- looking information, including, but not limited to: the ability to retain clients, renew existing contracts and obtain new business; an outbreak of contagious disease that could disrupt its business; the highly competitive nature of the industries in which Dexterra Group operates; reliance on suppliers and subcontractors; cost inflation; volatility of industry conditions could impact demand for its services; a reduction in the availability of credit could reduce demand for Dexterra Group’s products and services; Dexterra Group’s significant shareholder may substantially influence its direction and operations and its interests may not align with other shareholders; its significant shareholder’s 49% ownership interest may impact the liquidity of the common shares; cash flow may not be sufficient to fund its ongoing activities at all times; loss of key personnel; the failure to receive or renew permits or security clearances; significant legal proceedings or regulatory proceedings/changes; environmental damage and liability is an operating risk in the industries in which Dexterra Group operates; climate changes could increase Dexterra Group’s operating costs and reduce demand for its services; liabilities for failure to comply with public procurement laws and regulations; any deterioration in safety performance could result in a decline in the demand for its products and services; failure to realize anticipated benefits of acquisitions and dispositions; inability to develop and maintain relationships with Indigenous communities; the seasonality of Dexterra Group’s business; inability to restore or replace critical capacity in a timely manner; reputational, competitive and financial risk related to cyber-attacks and breaches; failure to effectively identify and manage disruptive technology; economic downturns can reduce demand for Dexterra Group’s services; its insurance program may not fully cover losses. Additional risks and uncertainties are described in Note 21 of the Corporation’s Consolidated Financial Statements for the years ended December 31, 2021 and 2020 contained in its most recent Annual Report filed with securities regulatory authorities in Canada and available on SEDAR at sedar.com. The reader should not place undue importance on forward-looking information and should not rely upon this information as of any other date. Dexterra Group is under no obligation and does not undertake to update or alter this information at any time, except as may be required by applicable securities law.